Advanced Research Administrators Training Series

Subawards and Subrecipient Monitoring

Subawards & Subrecipient Monitoring at UNH

Purpose of the Uniform Guidance Subaward Working Group:

- To document processes that already happen on campus

- Ensure compliance with new Uniform Guidance regulations

- Develop tools for research administrators on campus to assist in subaward monitoring and implementation of Uniform Guidance

What has been developed?

- Procedures for Subrecipient Invoice Processing by BSCs

- SPA Final Invoice Approval Process

- Just-In-Time Cost & Risk Analysis Form

- Subrecipient Risk Guide

- Subrecipient Monitoring Guide

Procedures for Invoice Processing by BSCs

Procedures for Invoice Processing by BSCs

Items to review:

- Performance Period

- Invoice frequency/sequencing

- Invoice amount & cumulative totals

- Invoiced amount details

- Certifications

- Payment

- Final Invoice

Procedures for Invoice Processing by BSCs: Certifications

Certifications:

Ensure the invoice contains institutional official signature and mandatory 2 CFR 200 415(a) certification language:

“By signing this report, I certify to the best of my knowledge and belief that the report is true, complete, and accurate, and the expenditures, disbursements and cash receipts are for the purposes and objectives set forth in the terms and conditions of the Federal award. I am aware that any false, fictitious, or fraudulent information, or the omission of any material fact, may subject me to criminal, civil or administrative penalties for fraud, false statements, false claims or otherwise. (U.S. Code Title 18, Section 1001 and Title 31, Sections 3729-3730 and 3801-3812).”

Procedures for Invoice Processing by BSCs: Certifications

Items to review (cont’d):

Certifications:

- Obtain PI approval and certification (electronically or in writing) prior to payment of the invoice.

Required language:

“I certify that any Subrecipient programmatic reports due during the period of time covered by this invoice have been received and are satisfactory, and that the listed expenses are appropriate and have my approval for payment.”

Procedures for Invoice Processing by BSCs: Payment

- Payment:

- must be made within 30 calendar days after receipt of invoice, unless the request is improper.

- if improper, resolve the issue through communication with the Subrecipient, the PI, or SPA as needed. Partial payment of the invoice may be made for those lines that are not in question if Subrecipient provides a revised invoice which excludes the lines in question.

Procedures for Invoice Processing by BSCs

Items to review (cont’d):

- Final Invoice:

- must be marked “final” and received within 45 days of the end of the subrecipient agreement.

- Verify with subrecipient authorized official that no more than $5,000 in residual unused materials remain as of the final invoice.

- Ensure the final invoice is not to be paid until the PI has received the final report from the Subrecipient.

- Forward the final invoice to SPA’s Subrecipient Agreement Coordinator for final approval, along with PI approval and subrecipient verification of residual unused materials.

- Once all approvals have been obtained, final invoice can be paid

Procedures for Invoice Processing by BSCs

Reminder:

Most invoices do not include a large amount of detail. Ask the subrecipient for back up documentation on specific budget line items if something does not appear correct. If there are any questions about the invoices, do not approve until all items are appropriately resolved.

Procedures for Subaward Final Invoice Processing by the Subrecipient Agreement Coordinator

Subaward Final Invoice Processing by SPA SAC

Items to review include, but are not necessarily limited to:

- Performance Period

- Invoiced amount and cumulative totals

- Invoiced amount details

- Certifications

Once invoice is deemed appropriate, the BSC will receive an e-mail from SAC with approval to pay. A copy of the invoice, along with significant correspondence will be filed on Xtender

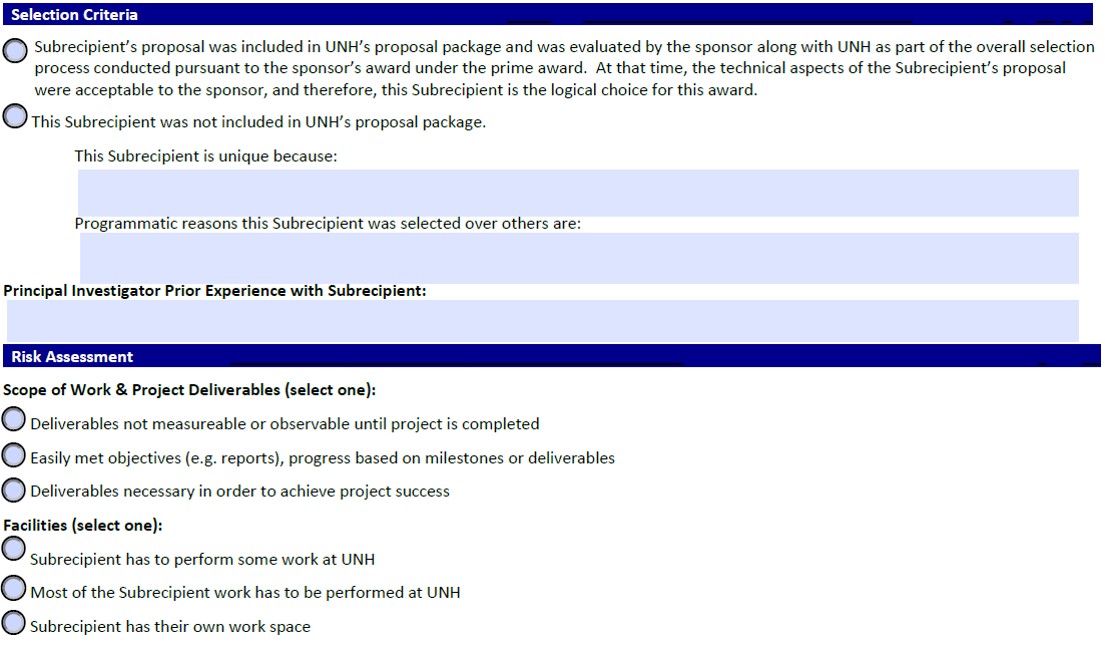

Just-In-Time Cost & Risk Analysis and Financial Risk Assessment Guide

Risk Levels

- Low: Subrecipient is sound and subaward does not introduce uncertainty into UNH’s own performance

- Medium: Subrecipient and/or subaward may impact UNH’s ability to complete the project

- High: Subrecipient and/or scope of work introduce potential for non-compliance with award terms and/or substantial uncertainty regarding UNH’s ability to complete the project

Aspects to Determine Appropriate Monitoring Procedures

- Percentage of prime award passed through to subrecipient

- Prior experience with subrecipient (entity has been a subrecipient of UNH before)

- Subrecipient financial status (for-profit/non-profit etc.)

- Award size relative to subrecipient’s sponsored research portfolio

- Scope of sponsor regulations, and the sensitivity/vulnerability of the research

- Evidence of appropriate administrative and financial controls

Risk Analysis

When rigorous oversight is necessary, SPA will work with PI to establish and maintain administrative monitoring procedures to enforce contractual requirements. These procedures/options may include:

- Fixed price agreement instead of cost reimbursable

- Tying payments to satisfactory technical progress reports

- Limited allotments of time and funds

- Site visits

- For entities not subject to A-133, back up documentation submitted with each invoice

Risk Analysis

UNH will not enter into a subaward if:

- Subrecipient is debarred or suspended

- PI has unresolved financial conflict of interest with subrecipient

- Subrecipient does not have adequate systems to account for award funds in accordance with federal requirements

Just-In-Time Cost & Risk Analysis and Financial Risk Assessment Guide

Just-In-Time Cost & Risk Analysis is used in conjunction with the Subrecipient Financial Risk Assessment Guide to determine the monitoring efforts necessary

Just-In-Time Cost & Risk Analysis

Purpose

- To document PI’s selection criteria considered when choosing a subrecipient

- Fiscal responsibility

- Ability to perform the scope of work

- Technical expertise

- Accessibility to technical/other necessary resources

Just-In-Time Cost & Risk Analysis

SPA will complete the top half of the document

Just-In-Time Cost & Risk Analysis

PI is responsible for completing Selection Criteria and Risk Assessment

Just-In-Time Cost & Risk Analysis

PI signature is required at the bottom of the document

Confirms PI’s consideration and review of subrecipient’s submitted scope of work, budget, and budget justification

Financial Risk Assessment Guide

- Completed by SPA

- Categories of risk considered along with information submitted in the Just-In-Time Cost & Risk Analysis:

- Organization type: university, non-profit, start-up etc.

- Foreign vs. domestic

- Prior experience with UNH

- Maturity of organization

- Audit report & accounting systems

Subrecipient Monitoring Guide

Subrecipient Monitoring Guide

- Programmatic and financial monitoring of subrecipients

- Responsible parties:

- Activity

- Pre-award

- At Time of Award

- Post award

Subrecipient Monitoring Guide

- PI Pre-award Procedures:

- PIs are responsible for developing proposals, including external collaborator(s) in accordance with sponsor requirements and proper classification of subrecipients and contractors

- Subrecipient vs. Contractor Checklist

- SPA Pre-award Procedures:

- Review PI’s classification of subrecipients and contractors

- Ensure subaward is appropriately included in the proposal

- Obtain necessary certifications

Subrecipient Monitoring Guide

- PI Time of award Procedures:

- Completion of new Just-In-Time Cost and Risk Analysis

- Define timelines for deliverables in order to meet project requirements

- Review terms of subaward to prepare oversight responsibility

Subrecipient Monitoring Guide

- SPA Time of award Procedures:

- Ensure completion of Just-In-Time Cost & Risk Analysis

- Perform restricted party screening

- Review subrecipient audit compliance

- Develop a subaward agreement based on risk designation

- Flow down application Terms & Conditions

- Determine specific risk profile and monitoring procedure for subrecipients

- Establish payment schedule

- Incorporate PI reporting requirements/deliverables

Subrecipient Monitoring Guide

- PI Post Award Procedures:

- Monitoring subrecipient progress

- Review of technical reports and expenses vs. budget

- Ensure subrecipient compliance with subaward agreement terms

- Along with the BSC, review subrecipient invoices for allowability, reasonableness, appropriateness of expenses

- Ensuring committed cost share is met/provided

- Approving/certifying only correct and appropriate invoices

Subrecipient Monitoring Guide

- SPA Post Award Procedures:

- Annual review of subrecipient risk profile

- Annual review of subrecipient single audit documentation

- Ongoing restricted party screening

- Audit of selected sample of subrecipient invoices

- High risk subrecipients

- May involve request for payroll records, records of consultant services, copies of paid invoices for items purchased, and travel

Invoice Processing: Real-Life Examples

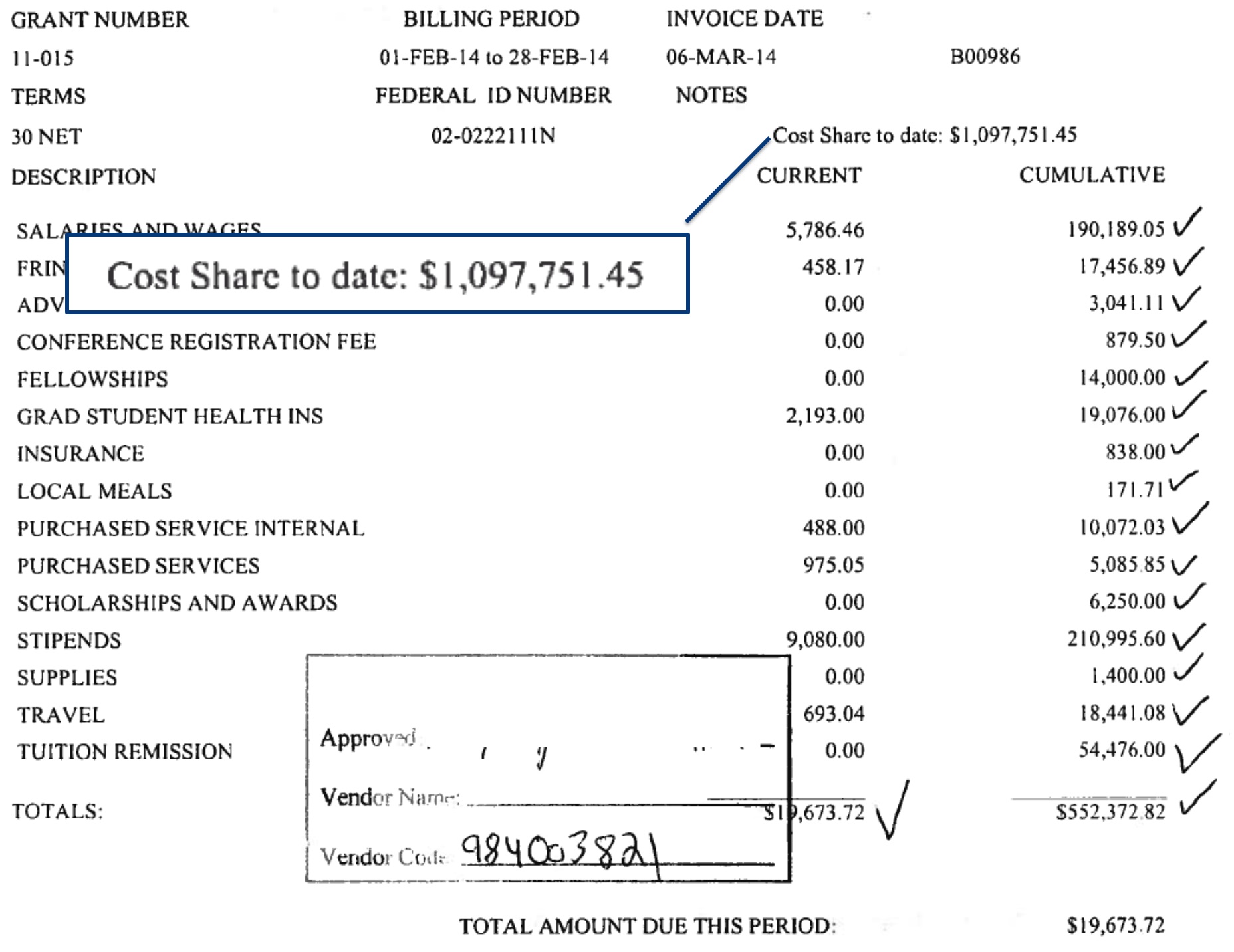

Cost Share - Invoice No. 36

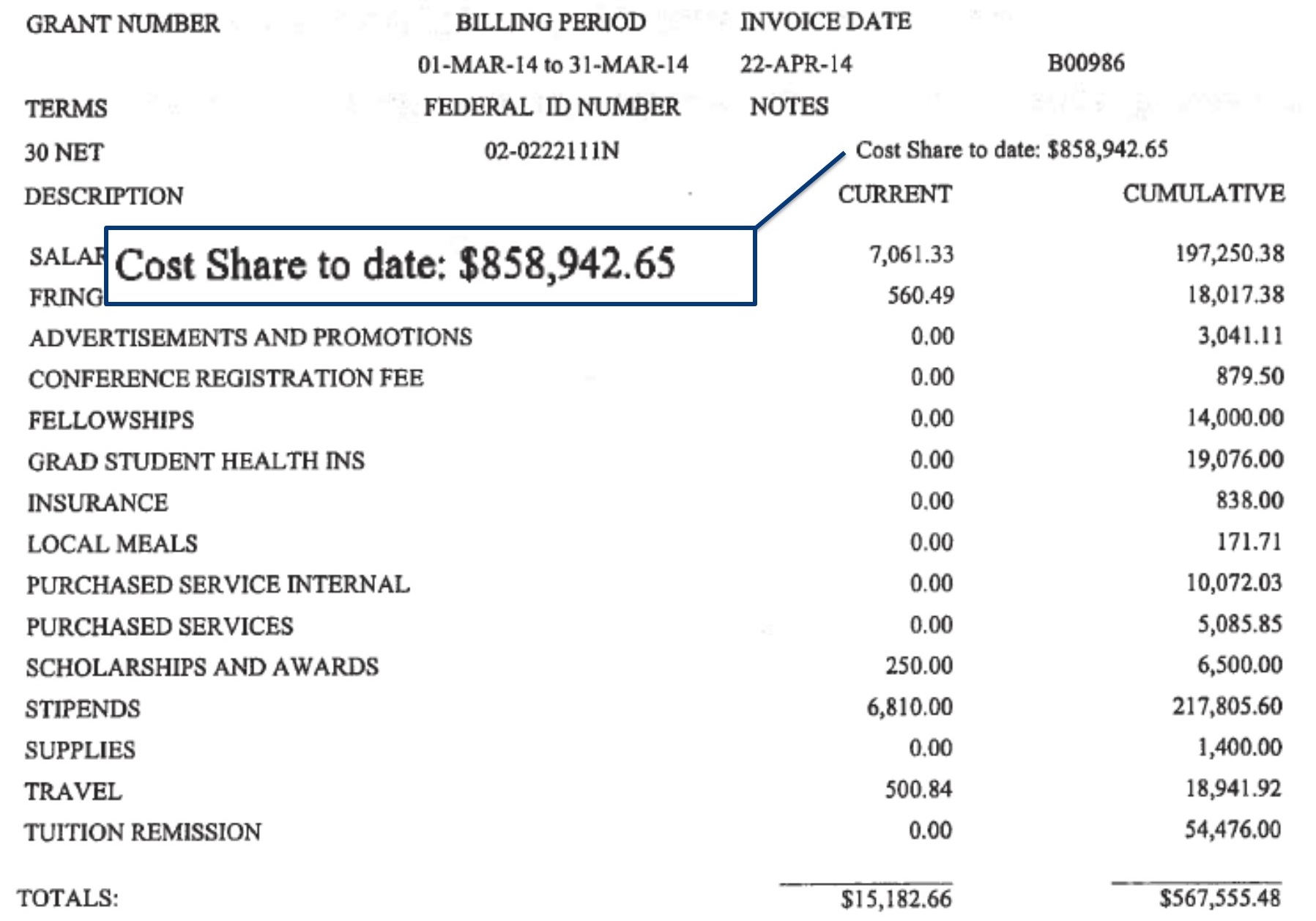

Cost Share - Invoice No. 37

Invoice Received

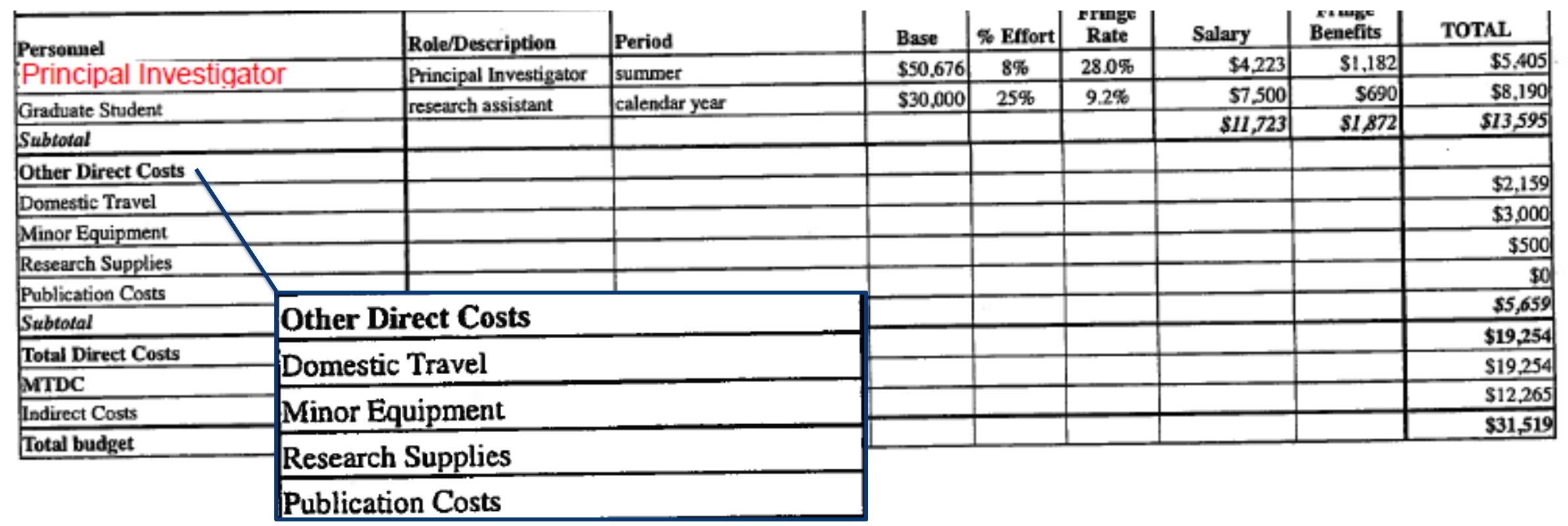

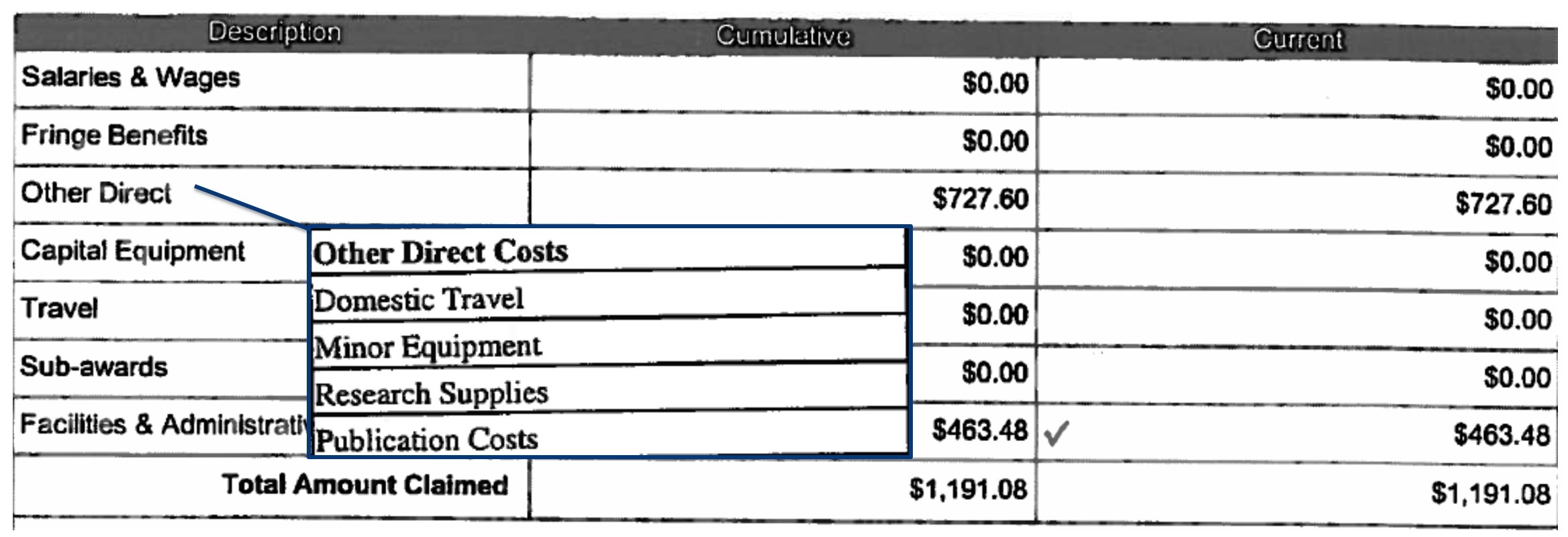

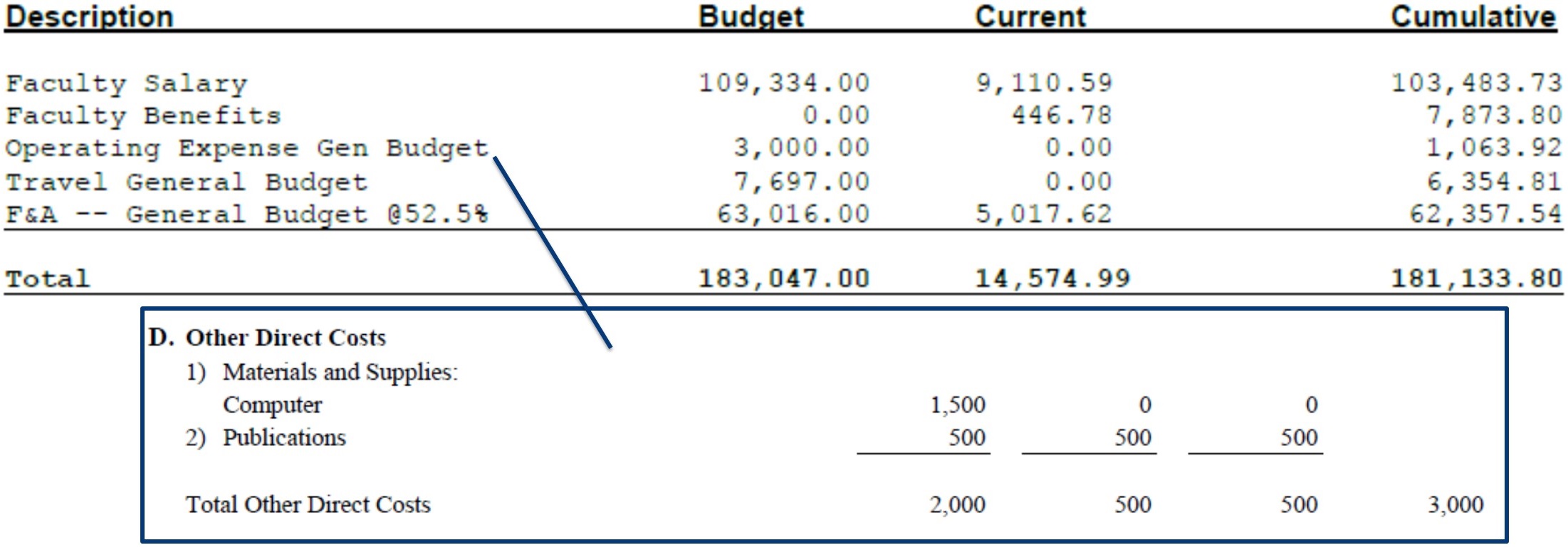

Other direct should be broken down per the subaward budget

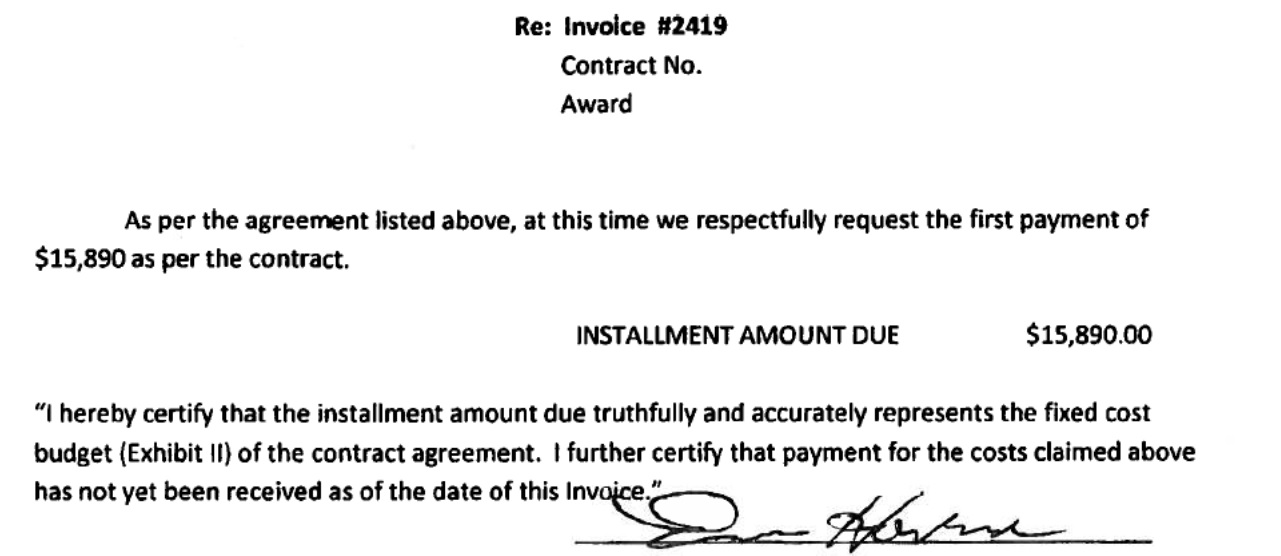

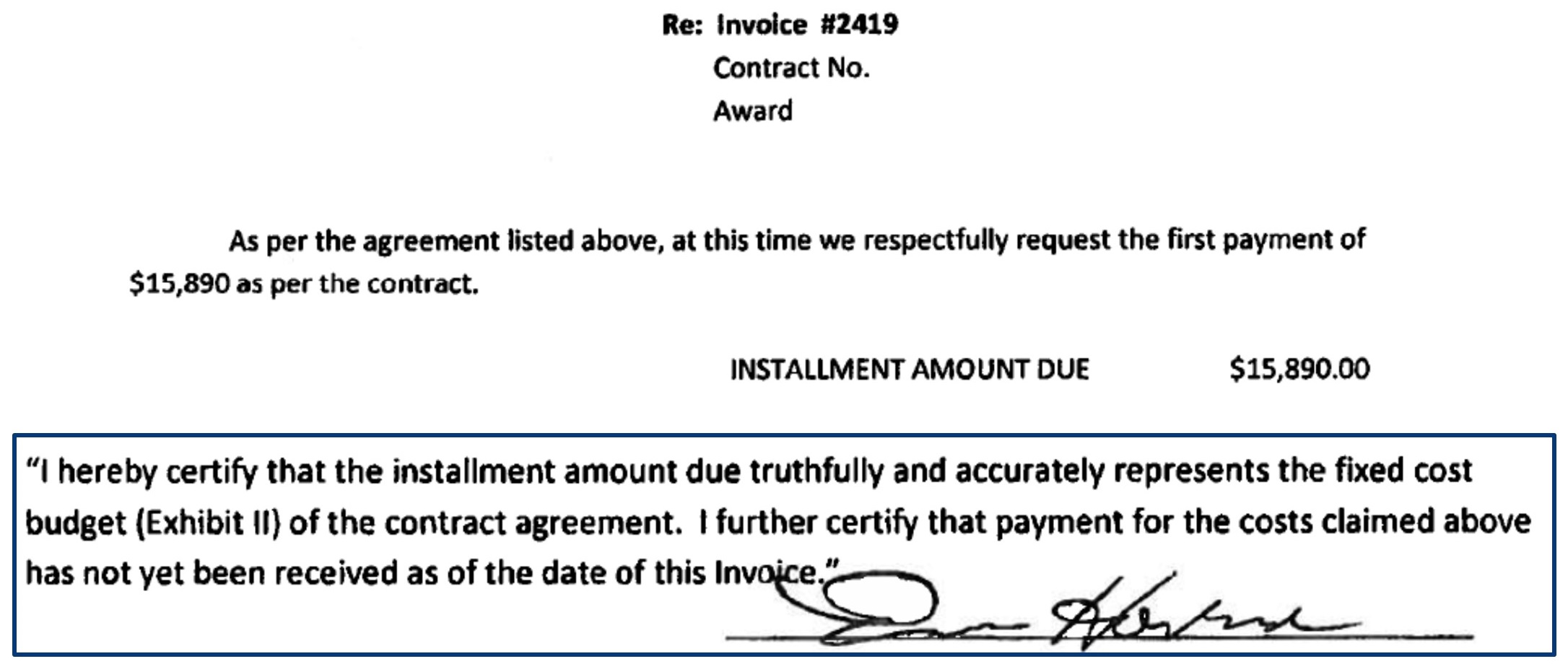

Certification Statement

Not using Uniform Guidance language

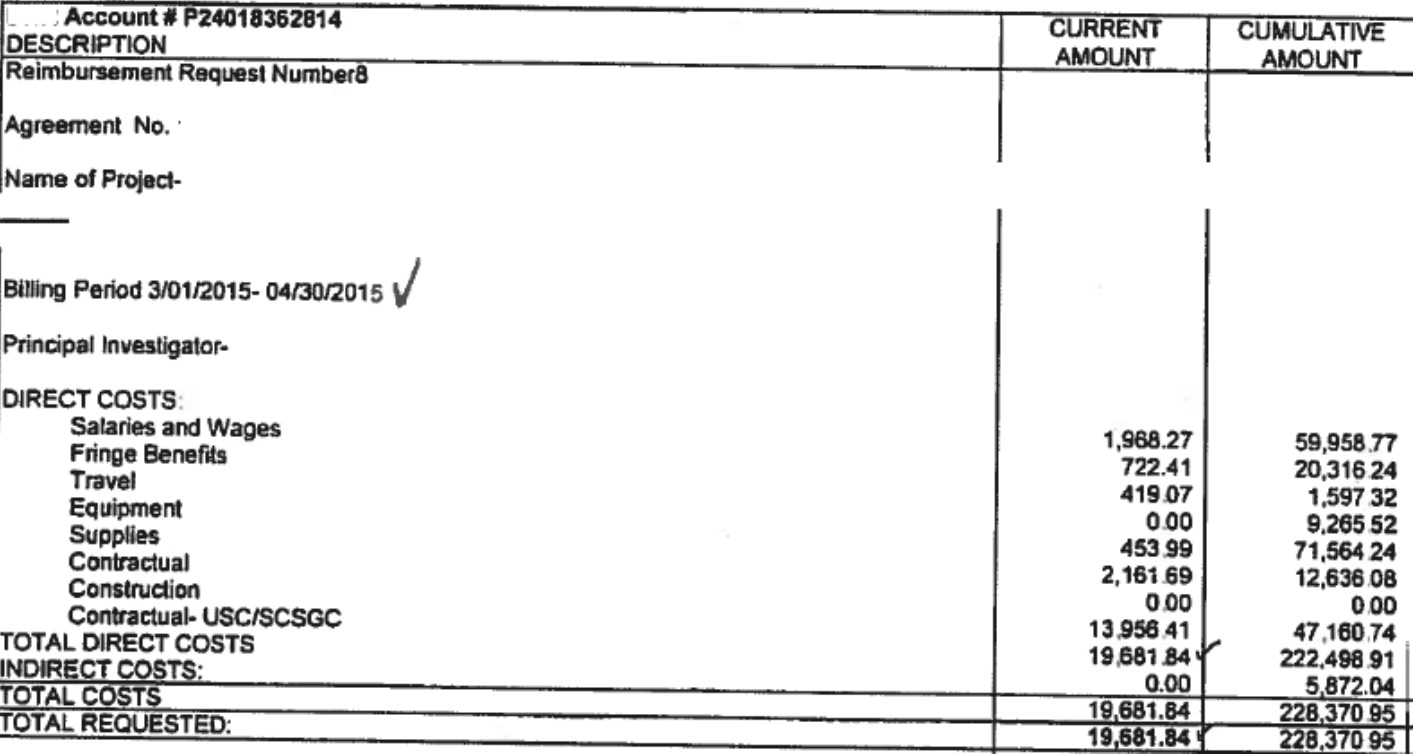

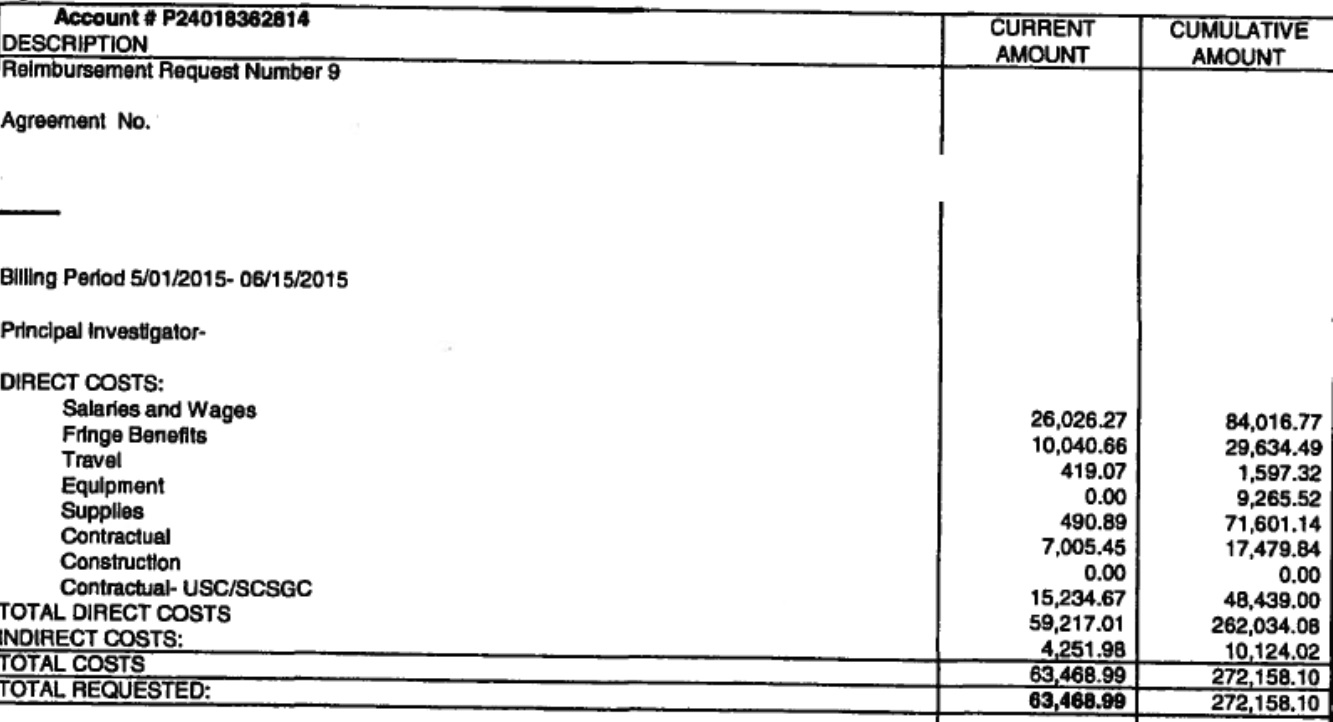

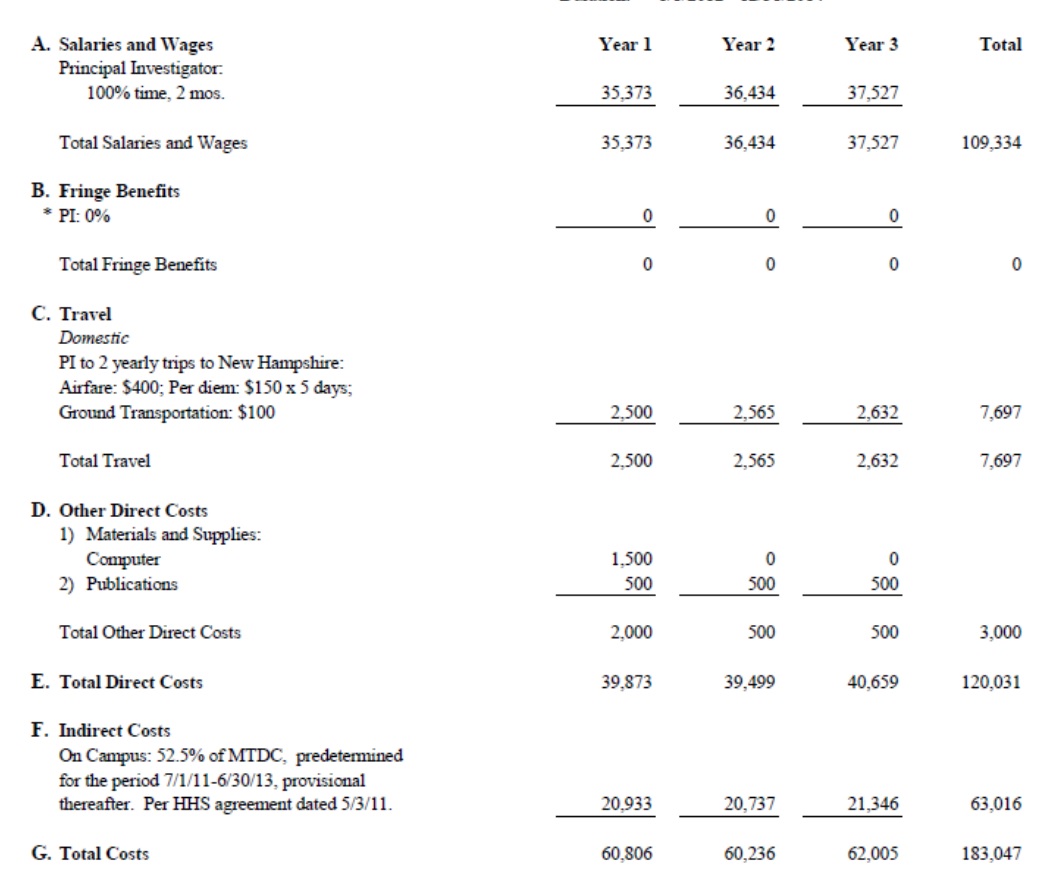

Cumulative Costs - Invoice 8

Cumulative Costs - Invoice 9

Thank you.

Questions?

Links to Subrecipient Monitoring and Management references in Uniform Guidance (2 CFR 200):

- Subrecipient Monitoring and Management 200.330, 331, 332

- Required Subrecipient Certification 200.415(a)